Hypothetical portfolio

Introduction

Creating a Portfolio

Modify an existing Portfolio composition

Changes in allocation

Start date of the Portfolio series

The total value of the portfolio

Show values at the end of each day, week, month or year

Show amounts in percentages or values

Securities contributions to the Portfolio performance

Employ the portfolio module to combine the series of two securities

Create a portfolio whose performance is equal to an index plus a certain

percentage

The folder which holds the files of each portfolio

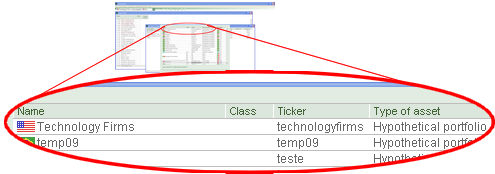

Introduction: The Hypothetical

portfolio module allows the user to choose a set of securities,

assign weights to each security and the system will create a historical

price serie for that portfolio. The portfolio will then become a member

of the list of securities in the system. In the example to the side, the

user created a portfolio called “Technology Firms”, and since the system

then treats this portfolio as any other security in the database, you

can then take advantage of all the resources in the system including:

graphs, highlights, technical indicators (Price change, volatility, etc),

use the portfolio as a benchmak, etc.

Introduction: The Hypothetical

portfolio module allows the user to choose a set of securities,

assign weights to each security and the system will create a historical

price serie for that portfolio. The portfolio will then become a member

of the list of securities in the system. In the example to the side, the

user created a portfolio called “Technology Firms”, and since the system

then treats this portfolio as any other security in the database, you

can then take advantage of all the resources in the system including:

graphs, highlights, technical indicators (Price change, volatility, etc),

use the portfolio as a benchmak, etc.

The

Type of asset assigned to hypothetical portfolios is Hypothetical

Portfolio

Any security available

in the Economatica database could be included in the hypothetical portfolios.

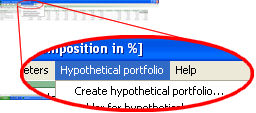

Creating a Portfolio: To create

a portfolio the user must open the Portfolio

Holdings module (to learn how to open a new module, consult chapter

Basic Structure > Getting started),

click the option Hypothetical Portfolio

and select Create Hypothetical portfolio

from the menu as shown on the side.

Creating a Portfolio: To create

a portfolio the user must open the Portfolio

Holdings module (to learn how to open a new module, consult chapter

Basic Structure > Getting started),

click the option Hypothetical Portfolio

and select Create Hypothetical portfolio

from the menu as shown on the side.

In the next

screen, the user should enter the portfolio name. The system will automatically

create a portfolio code (based on its name), however, if the user wishes

the code

can be changed.

In the next

screen, the user should enter the portfolio name. The system will automatically

create a portfolio code (based on its name), however, if the user wishes

the code

can be changed.

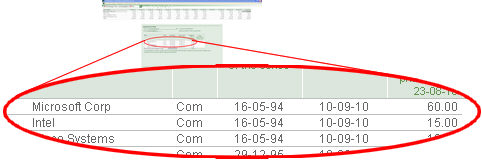

The user should

then create the list of securities that will comprise the portfolio. The

user can generate this list by pressing the <insert> key and picking

each security at a time. Aternatively, the user may also create a Stock

Guide with all the desired securities (consult chapter Stock

Guide > Filter), copy all the rows (ctrl C) in the Stock Guide

and then paste (ctrl V) into the portfolio editing screen.

The user should

then create the list of securities that will comprise the portfolio. The

user can generate this list by pressing the <insert> key and picking

each security at a time. Aternatively, the user may also create a Stock

Guide with all the desired securities (consult chapter Stock

Guide > Filter), copy all the rows (ctrl C) in the Stock Guide

and then paste (ctrl V) into the portfolio editing screen.

In the side example the

user chose the stocks of four technology companies for the portfolio.

After selecting

the securities the user must then enter the weight of each in the column

indicated on the side image. The weights must be assigned in percentage

terms and therefore the total sum must be equal to 100%.

After selecting

the securities the user must then enter the weight of each in the column

indicated on the side image. The weights must be assigned in percentage

terms and therefore the total sum must be equal to 100%.

In cases in which the portfolio

consists of many securities, it is possible to copy (ctrl C) the weights

from an external source (in case there is one) and paste them (ctrl V)

into the weight column of the portfolio editing screen.

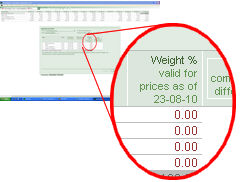

The user must

also inform the date for which the weights correspond. This is necessary

because weights valid for a certain date will not be valid for a different

date as the prices of the various securities will change across time in

an ununiform manner.

The user must

also inform the date for which the weights correspond. This is necessary

because weights valid for a certain date will not be valid for a different

date as the prices of the various securities will change across time in

an ununiform manner.

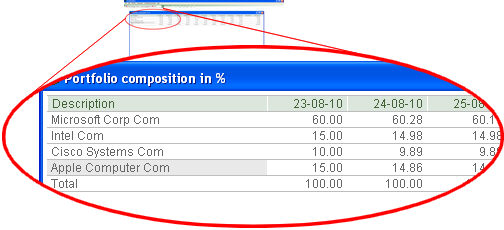

By entering the weights

at a certain date the user is indirectly informing the number of shares

held in each security. In the case on the side, for example, entering

the weight as 60% for the shares of Microsoft in the portfolio on 23/08/2010

can be interpreted as if $60 were invested in shares of that company in

that date, and, as the share price of Microsoft on 23/08/2010 was $24.28,

we can interprete that the portfolio has 2.47 shares of Microsoft ( 2.47

= 60 / 24.28).

This number will remain

constant across time. The weights of each security however change since,

as previously indicated, the prices of each security change ununiformly.

To inform

the reference date of the weights entered the user must click the mouse

right button over the weight column header and choose Change

Date from the menu.

To inform

the reference date of the weights entered the user must click the mouse

right button over the weight column header and choose Change

Date from the menu.

Once the user

selects the Save option in the editing

window (where the securities were selected and their weights entered)

a window will appear with the values of the portfolio day by day. In the

final topics of this chapter alternative options of displaying these values

will be described.

Once the user

selects the Save option in the editing

window (where the securities were selected and their weights entered)

a window will appear with the values of the portfolio day by day. In the

final topics of this chapter alternative options of displaying these values

will be described.

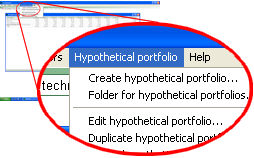

Modify an existing portfolio composition:

Follow the next steps to modify an existing portfolio composition:

Modify an existing portfolio composition:

Follow the next steps to modify an existing portfolio composition:

- a portfolio

holdings window must be open and must be the active window

- the portfolio being modified must be the Current

company (see chapter Basic Structure>

Change company)

- click Hypothetical Portfolio and

choose Edit hypothetical portfolio

from the menú (side image)

Changes in allocation: As

we have seen, by defining the composition on a given date, the user is

indirectly defining the number of shares held in each security, which

is a number that remains constant. The user, however, can make changes

to the number of shares held, in other words, define multiple compositions

in different dates so that the number of shares is constant only through

the date of the next composition.

Starting from the date of the new composition, new number of shares become

valid until the date of the next composition defined by the user and so

on.

Changes in shares held

are done without adding or taking out investments from the portfolio,

in other words, defining a new composition on date D, occurs as if all

of the securities in the old composition were sold (at the closing price

of date D) and the proceeds from the sale (neither more nor less) are

then used to acquire the new securities defined in the new composition

(bought also at the closing price of date D)

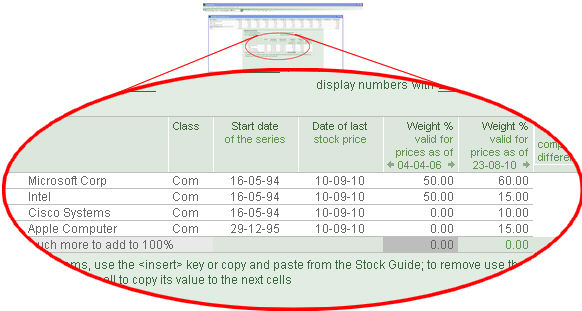

The oldest

composition defined by the user has a special treatment: in addition to

it being valid until the date of the next composition, it is also valid

going into the past. In the example to the side, the numbers defined as

of 04/04/2006 are valid from the beginning of the portfolio (see topic

Start date of the portfolio series

below) to the date of the next composition defined on 23/08/2010.

The oldest

composition defined by the user has a special treatment: in addition to

it being valid until the date of the next composition, it is also valid

going into the past. In the example to the side, the numbers defined as

of 04/04/2006 are valid from the beginning of the portfolio (see topic

Start date of the portfolio series

below) to the date of the next composition defined on 23/08/2010.

When there is only one

composition the numbers defined are valid from the start date of the portolio

to the end.

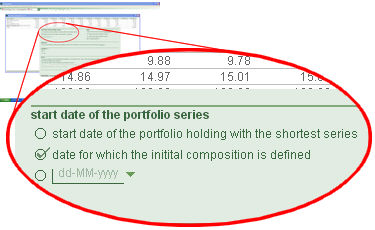

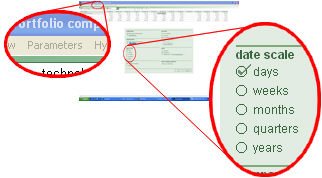

Start date of the portfolio series:

The user can choose the start date of the portfolio. After defining the

weight for each security click on tab Parameters

(as shown to the side).

Start date of the portfolio series:

The user can choose the start date of the portfolio. After defining the

weight for each security click on tab Parameters

(as shown to the side).

In the window

that will appear (side image) the user specifies the start date of the

portfolio series by selecting one of the options presented as illustrated

on the side.

In the window

that will appear (side image) the user specifies the start date of the

portfolio series by selecting one of the options presented as illustrated

on the side.

The total value of the portfolio: Even

though the user defines the portfolio composition by entering percentage

weight of each security, the system allows the user to enter the value

of the portfolio. This is done by clicking on the tab Parameters

as depicted on the side image.

The total value of the portfolio: Even

though the user defines the portfolio composition by entering percentage

weight of each security, the system allows the user to enter the value

of the portfolio. This is done by clicking on the tab Parameters

as depicted on the side image.

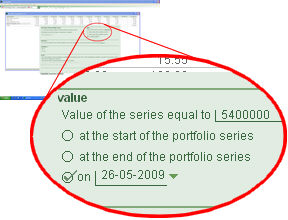

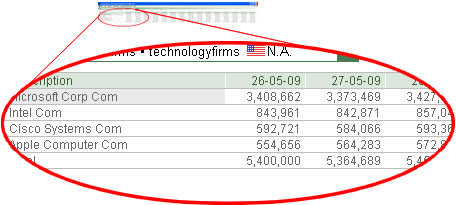

In the window

that will appear (side image) the user specifies the value of the portfolio

by selecting one of the options presented as illustrated on the side.

In the adjacent example, the user informed that the total investment value

of the portfolio on 26/05/2009 was $5,400,000.

In the window

that will appear (side image) the user specifies the value of the portfolio

by selecting one of the options presented as illustrated on the side.

In the adjacent example, the user informed that the total investment value

of the portfolio on 26/05/2009 was $5,400,000.

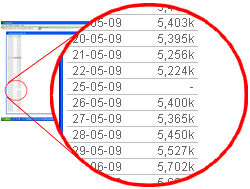

As can be

seen in the adjacent image (Stock

Prices window), the entire portfolio

series will be compatible with the investment value informed by the user.

As can be

seen in the adjacent image (Stock

Prices window), the entire portfolio

series will be compatible with the investment value informed by the user.

Show values at the end of each day,

week, month or year: Clicking the option Parameters

(shown on the side) brings up the parameters window which provides the

user the option to show the portfolio composition daily or at the end

of each week, month, quarter or year

Show values at the end of each day,

week, month or year: Clicking the option Parameters

(shown on the side) brings up the parameters window which provides the

user the option to show the portfolio composition daily or at the end

of each week, month, quarter or year

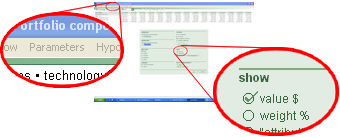

Show amounts in percentages or values:

Clicking the option Parameters (shown

on the side) brings up the parameters window which provides the user the

option of whether to view each security holding according to its percentage

weight or investment value.

Show amounts in percentages or values:

Clicking the option Parameters (shown

on the side) brings up the parameters window which provides the user the

option of whether to view each security holding according to its percentage

weight or investment value.

The investment

value of each security is a result of the definitions made by the user

as described in topic The total value of

the portfolio above. The side image shows investment values of

a portfolio whose value was assigned by the user to be $5,400,00 on 26-May-2009

The investment

value of each security is a result of the definitions made by the user

as described in topic The total value of

the portfolio above. The side image shows investment values of

a portfolio whose value was assigned by the user to be $5,400,00 on 26-May-2009

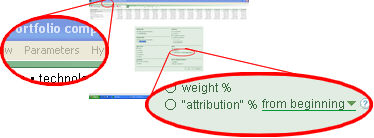

Securities contribution to the portfolio

performance: In addition to viewing the weight percentage or the

investment value in each security, it is also possible to see the performance

contribution of each security to the overall portfolio performance. The

contributions of each security depend on their individual return and weight

in the portfolio. To show contributions, the user must click on the option

Parameters (shown on the side), and

then choose the option Attribution %

in the parameters window as shown on the side image.

Securities contribution to the portfolio

performance: In addition to viewing the weight percentage or the

investment value in each security, it is also possible to see the performance

contribution of each security to the overall portfolio performance. The

contributions of each security depend on their individual return and weight

in the portfolio. To show contributions, the user must click on the option

Parameters (shown on the side), and

then choose the option Attribution %

in the parameters window as shown on the side image.

By clicking on the arrow

found in the right hand side of from beginning

the user reaches a window that provides the option to choose the period

for which to view the contributions.

The image

to the side shows a hypothetical portfolio whose start date was defined

by the user as 31/12/2009. The user chose to view the contribution of

each security since the start date.

The image

to the side shows a hypothetical portfolio whose start date was defined

by the user as 31/12/2009. The user chose to view the contribution of

each security since the start date.

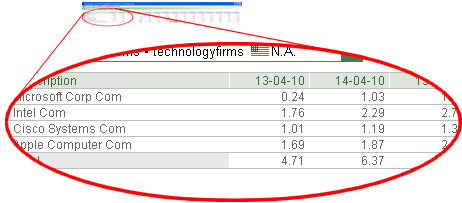

In this case, from the

start date until 13/04/2010, the portfolio returned 4.71%, that is, for

every $100 the portfolio earned $4.71, broken down as follows:

- 0.24 was earned from

the return produced by the shares of Microsoft in the portfolio

- 1.76 was earned from the return produced by the shares of Intel in the

portfolio

- 1.01 was earned from the return produced by the shares of Cisco in the

portfolio

- 1.69 was earned from the return produced by the shares of Apple in the

portfolio

Naturally, the contribution

of each security does not account for increases or decreases caused by

changes in allocation done by the user (see topic Changes

in allocation above)

Employ the portfolio module to combine the series of two

securities: There are cases in which a certain security is cancelled

and holders receive a different security in exchange. In such cases the

investor typically wishes to see historical prices which combine the old

security prices with the new security prices. The Hypothetical

portfolio module can be used for this purpose as explained below.

This combined series would

be the value of a portfolio that has 100% in the old security until the

date of the exchange and then 100% of the new security from that point

forward. Though the steps described earlier in this chapter can be used

to construct a portfolio with these specifications, the system offers

a simpler and quicker option to achieve this purpose of combining series.

Below we describe this alternative.

The user should

create a new portfolio following the steps discussed earlier, but after

providing the portfolio name the user should not insert any security into

the list of items in the portfolio. Rather, the user should click on tab

Ammend as shown in the side image.

The user should

create a new portfolio following the steps discussed earlier, but after

providing the portfolio name the user should not insert any security into

the list of items in the portfolio. Rather, the user should click on tab

Ammend as shown in the side image.

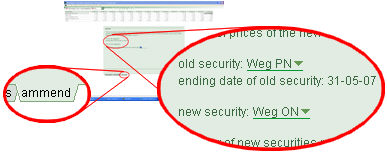

In the Ammend

window (side image), the user should simply specify the name of the old

security, the name of the new security and the exchange ratio. In the

example to the side, the security Weg PN ceased to exist on 31/05/2007

and its holders received in exchange the security Weg ON.

The investment value of

the portfolio constructed with the Ammend

tool is not defined the same way described in topic The

investment value of the portfolio above. Rather the investment

value of ammended series coincide with the value of the new security.

Create a portfolio whose performance is equal to an index

plus a certain percentage: The hypothetical

portfolio module allows the user to create a portfolio whose performance

is equal to an index (selected by the user) plus a certain percentage

amount (specified by the user). These types of series are frequently necessary

to be used as benchmarks.

To create

a portfolio with this characteristic the user should follow the steps

described earlier and create a portfolio where the desired index weight

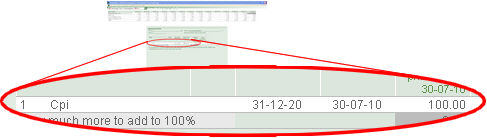

represents 100 % the portfolio. In the example to the side, the portfolio

is comprised 100% by the inflation index of the US (CPI).

To create

a portfolio with this characteristic the user should follow the steps

described earlier and create a portfolio where the desired index weight

represents 100 % the portfolio. In the example to the side, the portfolio

is comprised 100% by the inflation index of the US (CPI).

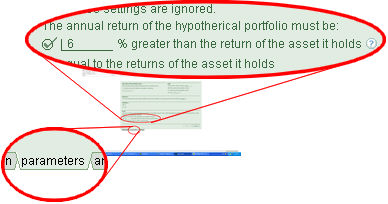

The user should

then click the tab Parameters (shown

on the side) and in the window that comes up enter the annual percentage

amount that the portfolio should return over the annual return of the

index. In

the example to the side, the user specified this amount as 6%. This means

that in a year in which the CPI returns 5%, the portfolio should return

11.3% (1.113 = 1.05 * 1.06).

The user should

then click the tab Parameters (shown

on the side) and in the window that comes up enter the annual percentage

amount that the portfolio should return over the annual return of the

index. In

the example to the side, the user specified this amount as 6%. This means

that in a year in which the CPI returns 5%, the portfolio should return

11.3% (1.113 = 1.05 * 1.06).

The folder which holds the files of each

portfolio: As explained earlier, the hypothetical portfolios created

by the user become part of the list of securities in the system’s database.

The folder which holds the files of each

portfolio: As explained earlier, the hypothetical portfolios created

by the user become part of the list of securities in the system’s database.

Each hypothetical portfolio

created by the user is saved in a file with extensión PTF. The portfolios

that are added to the list of securities in the system are those whose

files are located in the system’s portfolio folder. This system’s portfolio

folder can be viewed or changed by clicking the option

Hypothetical portfolio and choosing

Folder for hypothetical portfolios from the menu.